One of the most striking announcements in this week’s UK budget was the introduction of a new ‘soft drinks levy’ (quickly dubbed the sugar tax), which will come into force in 2018.

New taxes aren’t usually associated with the Behavioural Insights Team – partly because BIT’s preference is to find simpler, non-regulatory solutions before reaching for regulatory levers; but also because changing people’s economic incentives by imposing a tax is not a ‘nudge’ in the classic definition.

But we think that taxes can have an important role to play in encouraging behavioural change, especially when combined with other measures (think about the effect of tax on smoking). We also think that behavioural science can teach us a huge amount about how the levy should be implemented, and what its effects are likely to be.

And that’s what we’d like to focus on in this blog. Specifically on how two key groups – producers and consumers – are likely to respond to important design elements of the levy.

(i) How producers might respond to the levy

We often think about behavioural change in terms of how we influence individual behaviour. But there is growing recognition that the some of the biggest health benefits can be achieved through product reformulation by producers. For example, the gradual reductions of salt in processed foods, which have drastically cut salt consumption without consumers having to change their purchasing decisions.

Because it is already possible to replace sugar with low-calorie sweeteners, producers are likely to respond by reformulating their existing products. And we think that this will be where we are likely to see the biggest health impacts.

Two budget details give us a clue as to how this is likely to happen. The first is that the new levy will come into force in April 2018, giving producers two years to make gradual changes towards new, lower sugar levels. The second is the tiered nature of the tax, which means that producers are likely aim to reduce the sugar content of their products below the thresholds.

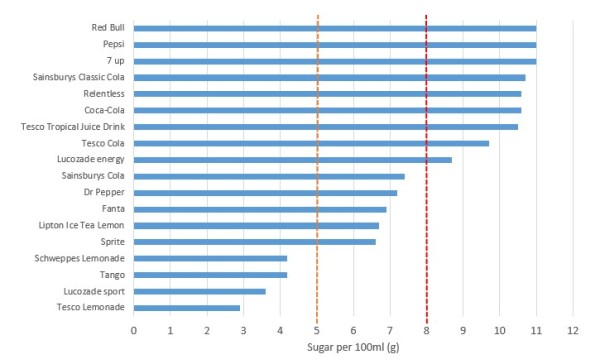

These thresholds are set at two different levels. Drinks with more than 5g of sugar per 100ml will face the levy. Drinks over 8g per 100ml, will face a higher levy. The chart below shows where a selection of sugary drinks currently sit. For many, a reduction of 10-20% in sugar content would be enough to shift them into the lower tier.

Source: BIT analysis

Two areas that are more uncertain, but which will also have an impact, are how producers and retailers decide to price and market different goods. The levy will likely have a greater impact on behaviour if the total, additional cost of a sugary drink is passed on to consumers, particularly where there is an obvious substitute (such as a ‘Zero’ version of the same brand). And it will also have a bigger impact if producers and retailers shift their marketing budgets to products lower in sugar, where they will in future likely enjoy higher margins.

(ii) How consumers might respond to the levy

How the producers and retailers react will have a knock-on effect on consumer behaviour – particularly in relation to the price of the products. From a purely economic perspective, we would obviously expect that the higher the differentiation in price, the greater the likelihood that individuals will substitute from a high to a lower sugar alternative (though note that, in a world in which reformulation takes place, we would also expect sugar content of those drinks with high sugar content to drop).

But the effect of price changes will likely be stronger if retailers make these changes more salient at the point of purchase. Research has shown that consumers underreact to taxes that are not salient. In one study by Raj Chetty in the US, posting tax-inclusive prices reduced demand by 8%, even though the same price was paid whether the tax was highlighted or not. In other words, if cans of cola are clearly marked as being higher in price because of the levy, this may lead to a greater effect on behaviour.

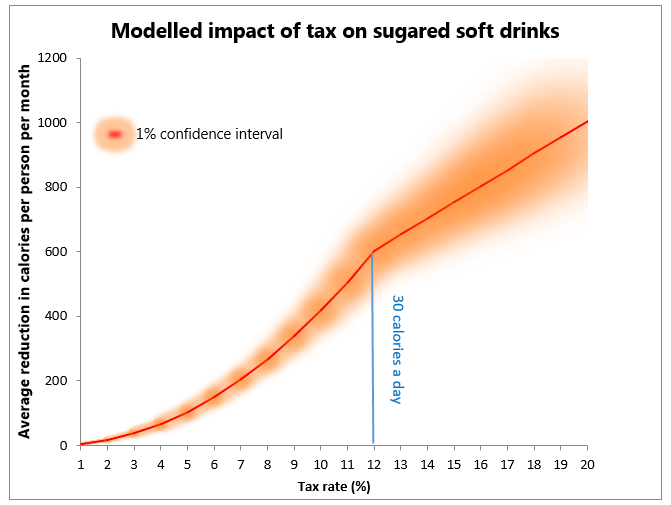

Within traditional economic price response there is also evidence that the effect on consumption may be disproportionately larger above a certain threshold. Previously we have modelled these effects and found a kink around a 12% price increase (see graph below), assuming of course that the price is passed onto consumers.

Source: BIT analysis

The final, and in some ways most elusive and interesting, effect of the sugar tax will be the signalling effects that the levy creates – namely that highly sugared drinks can be bad for your health, and that there are alternatives available. If this wider attitudinal change starts to change purchasing behaviours, we will be on the path towards reducing obesity in the UK.